The Top Mistakes People Make When Enrolling in Health Insurance

It should be a straightforward affair to choose a health insurance plan, but for the majority it is not the case. The similarities in the options, the confusion caused by the terminology, and the small errors that cost hundreds or even thousands of dollars every year to families are some of the factors that make this an arduous task. The bright side is that most of the enrollment difficulties are foreseeable, simple to avoid, and can be totally prevented if one gets the right kind of counseling. The very first thing one needs to do in order to steer clear of the most common mistakes people make when buying health insurance, is to see them for what they are, and this guide will very briefly recap the methods of making no error in simple language.

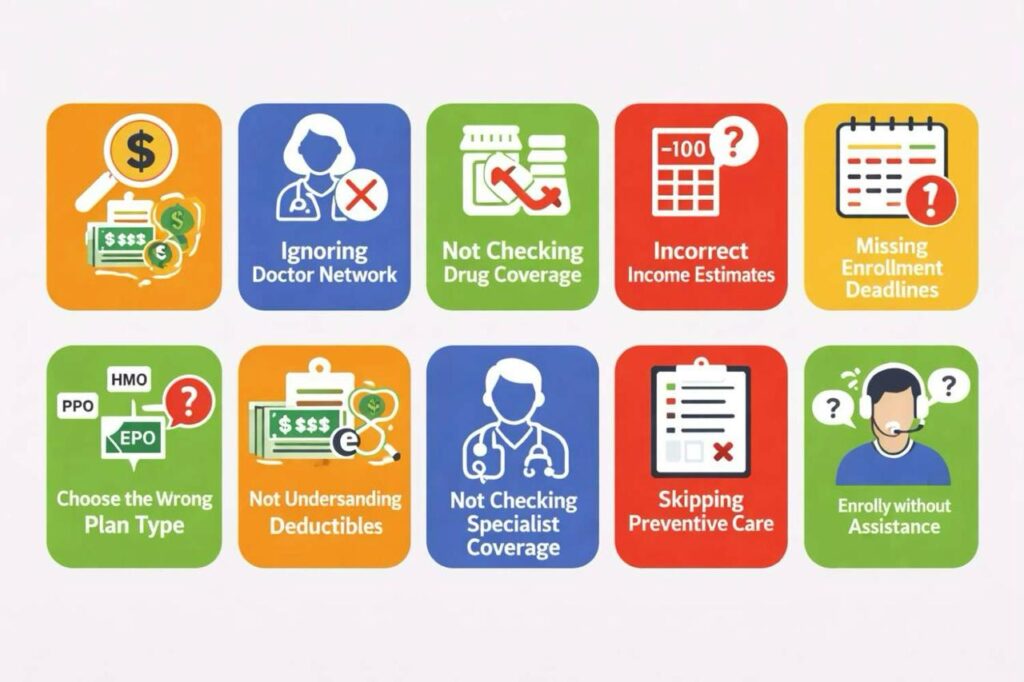

Mistake 1: The selection is based solely on the monthly premium

Usually, people select the plan with the minimum premium. It seems secure and economical. However, the majority of low-cost premiums are accompanied by:

- High deductibles

- High out-of-pocket costs

- Restriction in the network of providers

- High prices for medicine

A small premium is not the same as a low total cost, that is not the case always. Very often, the plan with the lowest monthly payment becomes the most expensive plan in the long run.

How to Avoid It:

Another low-yield choice stands out as soon as lumping all kinds of debts together as precedents prior to studying them into a meaningful schedule toward final decision making. You will not need to calculate the figures as Madrinas Insurance has done it for you and you can view the precise numbers.

Mistake 2: Ignoring the Provider Network

A number of people enroll in a plan medication with no knowledge of whether their doctors accept the plan or not since they automatically think it is a HealthNet plan. After that, when they go for their first check-up they find out that the doctor is out-of-network. Such a blunder can make a $40 copay turn into a $400 bill.

How to Avoid It:

Prior to signing up, verify:

- Your main doctor

- Your specialists

- Your child’s doctor

- The hospital you want

- Urgent care locations

We’ll check all that for you.

Mistake 3: Not Reviewing Prescription Drug Coverage

The list and pricing structure of medications this plan covers are different. Your medication might be:

- Not included

- Max pricing tier

- Authorisation needed

- Only generic versions available

You might be surprised at how much this can add to your yearly cost.

How to Avoid It:

Study the formulary of the plan before you get enrolled. Have a clear understanding if your medicines and dosages are going to be covered at a cost that you can predict.

Mistake 4: Underestimating or Overestimating Income

The subsidies provided by the Marketplace are based on your projected income, not the income stated in last year’s tax return. Wrong valuations cause the following:

- Incorrect subsidy amounts

- Higher monthly premiums

- Obrigaion to repay IRS in the future

How to Avoid It:

Estimate your income as realistically as possible. The Madrinas Insurance team is there to help you with the calculations and updates to keep your subsidies accurate.

Mistake 5: Missing Registration Deadlines

With few exceptions, insurance coverage and plans are unlikely to be available outside the open enrollment period.

How to Avoid It:

- Be aware of your deadlines

- Open Enrollment

- Special Enrollment (e.g., loss of coverage, moving, getting married, etc.)

With Madrinas Insurance, you can be sure that your application will be promptly submitted.

Mistake 6: Selecting the Incorrect Plan Type (HMO, PPO, EPO, POS)

Not every plan has the same characteristics. Every individual plan has its own set of rules and degree of flexibility.

HMO

Low cost, need referrals, and limited to in-network care.

PPO

Less rigid, high cost, and includes out-of-the-network access.

EPO

In-network only, however, no referrals are needed.

POS

Mixed plan with limited out-of-network benefits.

A wrong choice of plan type results in claimed denial, surprise bills, and dissatisfaction.

How to Avoid It:

Select according to your family’s healthcare usage rather than only considering the price.

Mistake 7: Not Understanding Deductibles and Out-of-Pocket Maximums

A deductible is the amount you have to pay before your insurance takes over the major services. However, many people misunderstand:

- What the deductible includes

- What it does not apply to

- • How the out-of-pocket maximum works for them

How to Avoid It:

Put these four numbers next to each other:

- Premium

- Deductible

- Copays

- Out-of-Pocket Limit

This is the principal piece of advice that saves you from surprise at the end of the year if you eventually need it.

Mistake 8: Not Learning About Specialist Coverage

Specialist visits are more expensive and may need a referral. Some plans even set a limit on how often one can see a specialist and which specialists one can visit.

How to Avoid It:

Check with insurance coverage for specialists prior to enrolling. This is critical for:

- Chronic illnesses

- Traumas

- Mental health care

- Pediatric needs

Mistake 9: Skipping Preventive Care Benefits

A lot of people that are enrolled in a health plan do not know that preventive services are free. If these services are not used, it is very likely that patients will end up with serious health problems and large bills.

Take advantage of your preventive services:

- Annual physicals

- Screenings

- Vaccinations

- Wellness check-ups

Mistake 10: Enrollment Without Professional Help

The whole procedure of signing up is purposely designed to be complicated. Hence, the probability of people is higher to:

- Pay more than necessary

- Pick plans that do not match their needs

- Bypass subsidy calculations

- Miss deadlines

- Wrongly report their income

All of these result in expensive mistakes.

How to Avoid It:

Licensed agents are your best choice. You can get various services at no cost from Madrinas Insurance such as plan comparison, network verification, prescription review, subsidy calculation, and enrollment help.

FAQ

What is the commonest error made in the process of choosing a health insurance plan?

The decision is made only considering the premium price. So, in the end, it piles up to the highest total cost.

If I end up with a wrong plan, can I switch to another plan?

Sure, you can do so either during the Open Enrollment period or if a qualifying life event happens.

How can Madrinas Insurance help you?

We will prepare a comparison of plans for you, verify the presence of your doctors in the network, ascertain the costs, and help you with any doubts.

Final Thoughts

Health insurance can influence a lot of things in life but it can also be a considerable source of stress—if not handled.wise. If you just keep clear of the mentioned mistakes, no issue will arise regarding your fami, budget, and peace of mind. The right direction will show you the plan that meets your requirements and does not cost too much.

Contact Madrinas Insurance now to compare plans and enroll with confidence.

Internal Links:

https://madrinasinsurance.com/health-insurance

https://madrinasinsurance.com/private-health-insurance

https://madrinasinsurance.com/contact