Obamacare vs Private Health Insurance: What’s Better for You in Texas?

People in Texas face a quandary between choosing Obamacare, also known as ACA (Affordable Care Act), and implementing private health insurance.

And the thing is most of these are not compared properly. They either decide that ACA is too complicated for them, or they presume that private insurance is much better. Either way, they cost you cash.

Edinburg and Rio Grande Valley, Texas both have houses in them. You’ll recognize both that are distinct and choose between them while avoiding spending too terribly.

Exactly, what is Obamacare (ACA)?

Obamacare is a governing body-regulated market creating income-based health insurance plans subsidized by subsidies.

The main benefit? The government chips in for each month’s payment when you are eligible.

These particular schemes are designed to have offers of essential health care components like:

- Preventive care

- Emergency services

- Prescription coverage

- Maternity and mental benefits

The Qualification for Buying Health Insurance

Private insurance is called private insurance because you earn it directly from any insurance company, not from the ACA marketplace.

No qualifying on income accompanies these plans. In other words, there are:

- No subsidies

- Higher premiums in most cases

- More flexibility in some plan structures

While private plans can usually offer benefits to particular situations, they are mostly more expensive.

Differences: Obamacare Versus Private Insurance

Cost

Obamacare:

Lower monthly premiums when qualified for subsidies

Private Insurance:

High monthly premiums with no financial assistance

Eligibility

Obamacare:

Based on income and household size

Private Insurance:

Available to anyone who can afford it

Coverage

Obamacare:

Standardized coverage with essential benefits

Private Insurance:

Can vary, sometimes more flexible but not always better

Approval

Obamacare:

Guaranteed acceptance regardless of pre-existing conditions

Private Insurance:

Some plans may have stricter approval guidelines

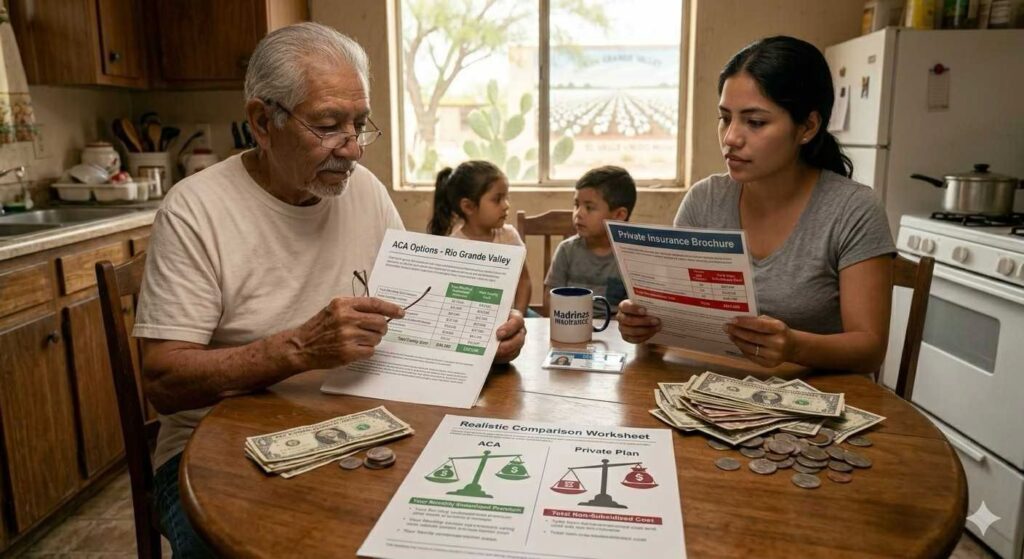

Real-World Comparison

Case 1: Single Adult, Age 35

Income: $32,000

ACA Plan: $25/month after subsidy

Private Plan: $280 per month

Case 2: Family of Four

Income: $58,000

ACA Plan: $180 per month

Private Plan: $1,100 per month

In both cases, ACA offers significantly lower costs.

When Private Insurance Might Make Sense

There are situations where private insurance is worth considering:

- High income with no subsidy eligibility

- Need for specific network providers not covered by ACA

- Preference for certain plan structures

In such circumstances, weighing out one ACA plan from the other would surely be wise.

Major Mistakes People Usually Commit

- Skipping ACA eligibility check

- Assuming private is “better” without comparing cost

- Choosing based only on monthly premium

- Not reviewing coverage details

These things usually result in overpaying or in worse cases failing to get the right coverage.

How to Choose the Best One in Your Line

The decision comes down to three things:

- Your income

- Your healthcare needs

- Your budget

In general, ACA plans tend to be most cost-effective. The only way to determine this, however, is by looking at your plan.

Highlights

- Less expensive plans usually: ACA plans

- Private insurance can be useful in specific cases

- Cost differences can be significant

- Always compare before choosing

- Expert advice helps you avoid many and expensive mistakes

FAQ’s

Is Obamacare more affordable than private insurance?

For the most part, in subsidized fashion, the plans under ACA are much cheaper.

Can I have both ACA and private insurance?

No, you typically choose one based on your needs.

Is private insurance better coverage?

Not necessarily. ACA plans include essential benefits that many private plans also offer.

What is the best option for families?

Most families benefit more from ACA due to lower costs.

Call to Action

Before choosing a plan, make sure you compare your real options based on your situation.